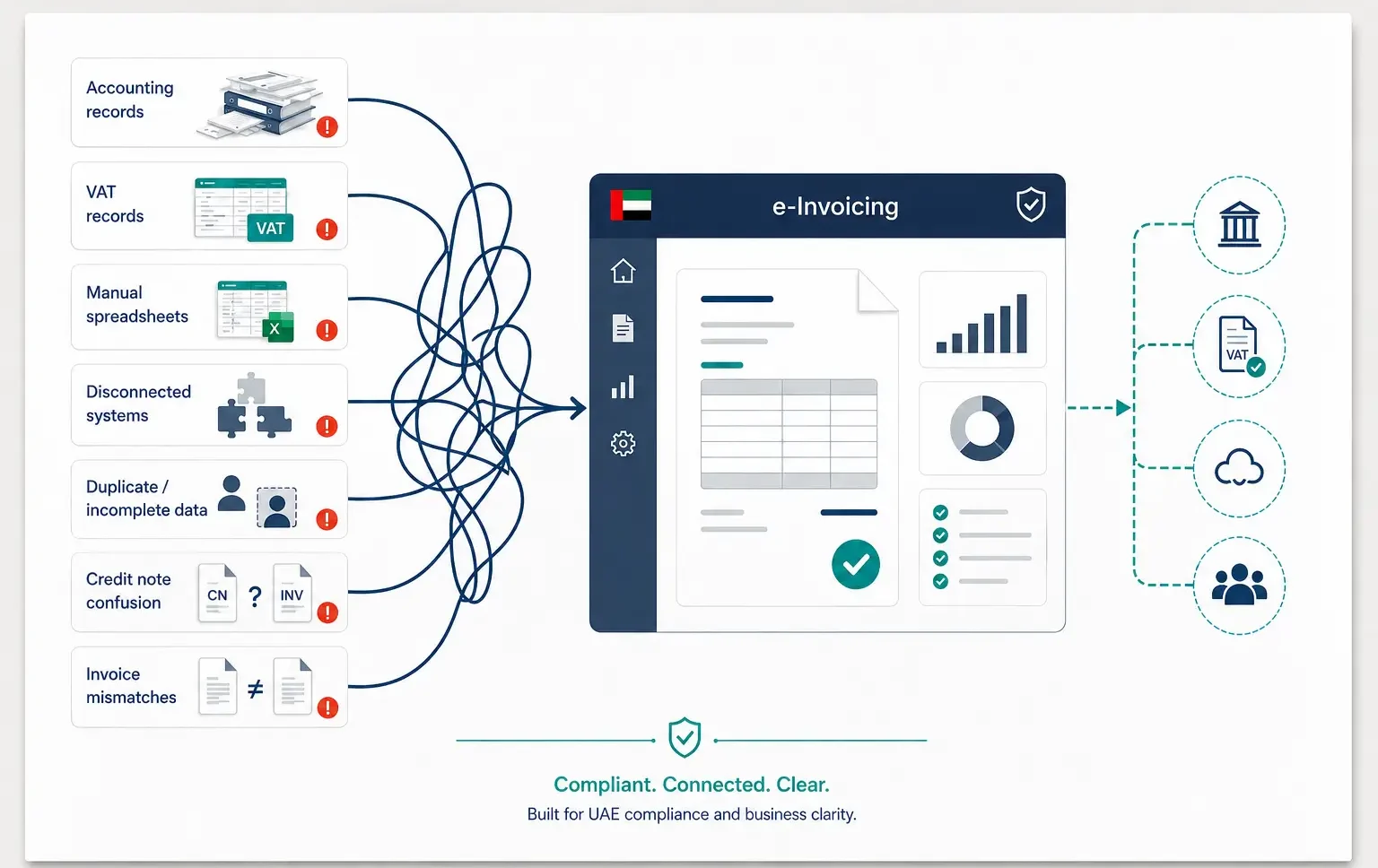

UAE e-invoicing is not only a software change. It will affect how businesses issue invoices, record VAT, manage customer details, handle supplier invoices, process credit notes, and reconcile VAT returns.

Many businesses may think the main task is choosing an e-invoicing provider. In practice, the bigger task is usually cleaning the data behind the invoices.

If customer names are inconsistent, TRNs are missing, VAT codes are wrong, credit notes are not linked to original invoices, or VAT returns do not match accounting records, e-invoicing can make these issues more visible.

This guide explains what UAE businesses should review before e-invoicing becomes mandatory, especially from a VAT and accounting point of view.

What Should Businesses Fix Before UAE e-Invoicing?

Businesses should start with invoice data, VAT codes, customer records, supplier records, accounting systems, credit notes, and VAT return reconciliation.

| Area to Fix | Why It Matters |

|---|---|

| Customer records | Wrong legal names, missing TRNs, or outdated details can create invoice issues |

| Supplier records | Supplier invoices must support input VAT and accounting entries |

| VAT codes | Wrong VAT treatment can affect VAT returns and tax reporting |

| Invoice numbering | Duplicate or missing invoice numbers weaken the audit trail |

| Credit notes | Refunds, discounts, and corrections must link back to original invoices |

| Accounting software | The system should handle invoice data, VAT records, and reporting correctly |

| Approval process | Invoices should be checked before they are issued, not corrected later |

| VAT reconciliation | VAT returns should match invoice records and accounting ledgers |

| Manual invoices | Excel and PDF-based processes may increase data errors |

| ASP readiness | An Accredited Service Provider can work better when the source data is clean |

The businesses most ready for e-invoicing will not be the ones that choose software first. They will be the ones that clean their invoice and VAT data first.

Need VAT Guidance?

Not sure what to do next with VAT?.

Ask our team first and get a clear answer for your business situation.

e-Invoicing Is Not Just a PDF Invoice by Email

A PDF invoice sent by email is not the same as an e-invoice.

An e-invoice is a structured electronic invoice that can be issued, exchanged, received, and processed through the required system. It is not only about how the invoice looks. It is about whether the invoice data can be read, exchanged, matched, corrected, and reconciled.

This matters because invoice data affects VAT reporting. If the invoice includes the wrong TRN, wrong VAT rate, wrong supply date, or wrong customer details, the issue may move through the accounting records and affect VAT filing.

Many businesses may spend time improving the invoice design. That is useful, but it is not enough. The real test is whether the invoice data is complete and accurate.

Who Is Actually Affected by UAE e-Invoicing?

UAE e-invoicing is expected to affect businesses involved in in-scope business transactions, especially B2B and B2G transactions. This means it is not only a concern for large companies.

| Business Type | Why It Should Prepare |

|---|---|

| VAT-registered SMEs | VAT invoices, input VAT, output VAT, and filing depend on clean invoice records |

| Large companies | They have earlier implementation timelines and more complex system needs |

| Government suppliers | B2G transactions are expected to fall within the e-invoicing system |

| Trading companies | Imports, exports, supplier invoices, and VAT treatment must be recorded properly |

| Service companies | Customer location, service description, and VAT treatment must be clear |

| Businesses using Excel invoices | Manual invoice numbering and missing data can create problems |

| Businesses with many credit notes | Refunds, discounts, and corrections must be traceable |

Even if the business is not in the first implementation phase, it should use the time before 2027 to clean its records.

UAE E-Invoicing Timeline: Who Must Act First?

The implementation will happen in phases. Large businesses need to prepare earlier, while smaller businesses have more time.

| Business Category | ASP Appointment Deadline | Implementation Date |

|---|---|---|

| Pilot group | Pilot starts 1 July 2026 | Selected taxpayers only |

| Businesses with annual revenue of AED 50 million or more | 30 October 2026 | 1 January 2027 |

| Businesses below AED 50 million revenue | 31 March 2027 | 1 July 2027 |

| In-scope government entities | 31 March 2027 | 1 October 2027 |

The deadline is not the date to start preparation. It is the date by which weak invoice data, system gaps, and VAT record issues should already be fixed.

The Real Risk: Bad Data Will Move Faster After e-Invoicing

Before e-invoicing, a wrong invoice may stay inside accounting records until VAT filing, audit review, customer checking, or supplier reconciliation.

With e-invoicing, invoice data becomes more structured. This can make errors easier to detect and harder to ignore.

Common issues may include:

- wrong customer TRN

- wrong supplier TRN

- wrong VAT rate

- wrong invoice date

- wrong supply date

- duplicate invoice number

- missing credit note reference

- invoice issued under the wrong company or branch

- invoice posted to the wrong VAT code

- supplier invoice not matched with the accounting entry

E-invoicing does not create the VAT mistake. It can expose the mistake earlier.

What Invoice Fields Should Businesses Clean First?

Businesses should review the invoice fields that affect VAT, accounting, customer records, and reporting.

| Invoice Field | What Can Go Wrong |

|---|---|

| Legal name | The customer or supplier name does not match official records |

| TRN | The TRN is missing, wrong, or outdated |

| Invoice number | Numbers are duplicated, skipped, or manually changed |

| Invoice date | The invoice falls into the wrong VAT period |

| Supply date | The VAT timing may be affected |

| Description | The goods or services are too vague to support VAT treatment |

| VAT rate | The supply is treated under the wrong VAT category |

| VAT amount | The VAT calculation does not match the invoice value |

| Credit note link | The credit note is not linked to the original invoice |

| Currency | Foreign currency invoices are not recorded consistently |

| Branch or entity name | The invoice is issued under the wrong licence, branch, or entity |

For many SMEs, this review is more useful than comparing software features. These are the fields that create daily VAT and accounting issues.

Customer and Supplier Records Will Become a VAT Control Point

Customer and supplier records are often treated as basic admin data. Under e-invoicing, they become more important.

These records usually include the legal name, TRN, address, contact details, payment terms, and accounting codes of each customer or supplier.

Common master data issues include:

- one customer created more than once

- supplier name written differently from the trade licence

- missing TRN

- old address details

- inactive suppliers still used in the accounting system

- UAE customers mixed with overseas customers

- related-party suppliers not clearly identified

- wrong account codes attached to customers or suppliers

If master data is weak, every invoice created from that data can carry the same mistake.

Credit Notes May Become One of the Biggest Problem Areas

Credit notes are often where VAT mistakes appear. This can happen when a business gives a refund, cancels an invoice, reduces the price, gives a post-sale discount, or corrects an invoice error.

Every credit note should clearly connect to the original invoice. The reason for the credit note should also be clear.

| Credit Note Situation | What Businesses Should Check |

|---|---|

| Invoice cancelled | The original invoice reference is clear |

| Partial refund | The VAT amount is adjusted correctly |

| Discount after invoice | The reason and calculation are documented |

| Wrong invoice amount | The correction can be traced |

| Wrong VAT treatment | The accounting entry and VAT return are corrected |

| Customer dispute | The approval and reason are documented |

If credit notes are not controlled properly, the VAT return may show the wrong output VAT or adjustment figures.

How Can E-Invoicing Affect VAT Return Filing?

VAT return filing depends on the quality of invoice data.

Output VAT comes from sales invoices. Input VAT comes from supplier invoices. Credit notes affect adjustments. Invoice dates and supply dates can affect the reporting period. VAT codes affect how transactions appear in the VAT return.

If these records are wrong, the VAT return may still be filed, but the figures may not be properly supported.

The VAT return will only be as reliable as the invoice data feeding it.

Businesses that already struggle with invoice matching, input VAT support, credit notes, imports, reverse charge entries, or accounting reconciliation should review their process before e-invoicing becomes mandatory.

How Can e-Invoicing Affect VAT Accounting?

E-invoicing will make accounting quality more important because invoice data must connect with ledgers, VAT codes, customer records, supplier records, and VAT return figures.

Businesses should review:

- VAT codes in the accounting system

- sales invoice posting rules

- supplier invoice posting rules

- customer and supplier ledgers

- credit note matching

- import and reverse charge entries

- zero-rated and exempt supplies

- bank reconciliation

- approval controls

- user access inside accounting software

The accounting team should not wait for the IT team to solve every issue. VAT codes, ledger mapping, customer data, supplier data, and credit note controls are accounting responsibilities before they become software settings.

Why Excel Invoices and Manual PDFs May Become a Problem

Manual invoices are not automatically wrong. Many small businesses use Excel, Word, or PDF invoice templates. The issue is whether the invoice data is controlled, consistent, traceable, and ready for structured exchange.

Manual invoice processes often create problems such as:

- duplicate invoice numbers

- missing TRN fields

- inconsistent customer names

- wrong VAT calculations

- weak approval trail

- missing credit note references

- different invoice templates used by different staff

- poor reconciliation with VAT returns

Businesses that rely on manual invoicing should review the process early. The aim is not only to change the invoice format, but to reduce errors before they become part of the reporting system.

What Should SMEs Do Before Choosing an Accredited Service Provider?

An Accredited Service Provider can help transmit and process invoice data through the e-invoicing system. However, it cannot automatically fix wrong VAT treatment, poor customer records, missing supplier TRNs, or weak accounting controls.

Before choosing an ASP, SMEs should:

- Clean customer and supplier records.

- Review invoice fields.

- Fix VAT codes in the accounting system.

- Review the credit note process.

- Reconcile VAT returns with accounting ledgers.

- Check duplicate customers and suppliers.

- Identify manual invoice processes.

- Check whether the current software can export or connect invoice data.

- Assign one finance owner and one system owner.

- Prepare a simple implementation timeline.

An ASP connection works better when the business has already cleaned the records that feed the system.

What Questions Should You Ask Before Appointing an ASP?

Businesses should not select an ASP only based on price or software name. They should ask practical questions about accounting, VAT, support, errors, and records.

- Are you accredited or in the accreditation process?

- Which accounting systems do you integrate with?

- How will invoice errors be handled?

- How will credit notes link to original invoices?

- How will customer and supplier TRNs be validated?

- What happens if invoice transmission fails?

- What reports or dashboards will the business receive?

- How long will invoice records be archived?

- Who handles support, the finance team or IT team?

- Can the system handle multiple branches or entities?

- How are user access rights controlled?

These questions help the business understand whether the provider fits the actual accounting and VAT process.

What Should Finance Teams Review Before 2027?

Finance teams should not wait until the implementation date. A simple internal review can show whether the business is ready or whether the invoice process needs correction.

| Question | Why It Matters |

|---|---|

| Do our VAT returns match the ledgers? | This helps prevent filing and reconciliation gaps |

| Are customer TRNs complete? | This reduces invoice processing issues |

| Are supplier invoices valid? | This supports input VAT recovery |

| Are credit notes controlled? | This helps prevent wrong VAT adjustments |

| Are invoice numbers sequential? | This strengthens the audit trail |

| Are VAT codes correct? | This prevents wrong output VAT or input VAT treatment |

| Are overseas customers classified correctly? | This helps with zero-rated or outside-scope treatment |

| Do we use multiple systems? | This reduces data mismatch risk |

What Should Businesses Not Wait Until 2027 to Fix?

Some issues take time to correct because they affect daily accounting habits. Businesses should not leave these matters until the e-invoicing deadline is close.

- wrong VAT codes

- missing TRNs

- duplicate customers

- duplicate suppliers

- unmatched supplier invoices

- credit notes without original invoice reference

- manual invoice numbering

- unreconciled VAT control accounts

- invoices issued from different templates

- old customer and supplier records

- weak approval controls

- poor separation of taxable, zero-rated, exempt, and outside-scope supplies

These are not only e-invoicing issues. They are VAT and accounting control issues.

UAE e-Invoicing Readiness Checklist

e-Invoicing Readiness Checklist

- Review current tax invoice format

- Check legal names, TRNs, addresses, and invoice fields

- Clean customer and supplier master data

- Review VAT codes in the accounting system

- Check invoice numbering and sequencing

- Review credit note and refund process

- Reconcile VAT returns with accounting records

- Identify manual invoice processes that may create errors

- Check whether accounting software can support structured invoice data

- Prepare questions before appointing an ASP

- Monitor official e-invoicing updates and provider announcements

When Should a Business Get VAT Accounting Readiness Support?

A business should consider support if the accounting and VAT records are not yet clean enough for structured invoice reporting.

This may be useful when:

- VAT returns do not match ledgers

- invoices are issued manually

- customer TRNs are missing

- supplier records are duplicated

- credit notes are not linked properly

- imports and reverse charge entries are frequent

- the finance team uses spreadsheets for invoicing

- the business has multiple branches or systems

- tax invoices do not follow one format

- input VAT claims are not well supported

If your business wants to prepare before UAE e-invoicing becomes mandatory, a VAT accounting review can help identify gaps in invoice data, VAT codes, customer records, supplier details, credit notes, and return reconciliation.

Our team can review your VAT accounting records, invoice data, and compliance process so your business can understand what should be corrected before implementation.

Final Summary

UAE e-invoicing should not be treated as a last-minute software project. It will affect invoices, VAT records, accounting systems, customer data, supplier records, credit notes, and VAT return reconciliation.

The most prepared businesses will be the ones that clean their invoice data before the deadline. This includes correcting customer and supplier records, checking TRNs, reviewing VAT codes, controlling credit notes, improving invoice numbering, and reconciling VAT returns with accounting records.

Large businesses need to prepare earlier, but SMEs should not wait until 2027 to start. The earlier a business reviews its VAT and accounting records, the easier the transition is likely to be.

Need VAT Guidance?

Not sure what to do next with VAT?.

Ask our team first and get a clear answer for your business situation.