A tax invoice can be defined as a written document that proves the occurrence of taxable supplies and their details. An original copy of this invoice is delivered by VAT-registered business to the recipient, and the VAT-registered business can keep the invoice in the event that there is no recipient. VAT invoices must be issued for all taxable sales. and all tax invoice requirements must be contained correctly and completely in the invoice to avoid any penalties or fine might be applied for Federal Tax Authority. In this article we will clarify all what you need to know about requirements for Issuing a tax invoice in the UAE.

UAE VAT Invoice Requirements

There are two different kinds of tax invoices in UAE; simplified and detailed.

Simplified Tax Invoice Requirements in UAE

Simplified tax invoices are for supplies that are less than the Federal Tax Authority’s predetermined amount of AED 10,000. They are issued when clients or customers are retail buyers without any Tax Registration Number (TRN). A simplified VAT invoice in the UAE is for the retail industry, including supermarkets.

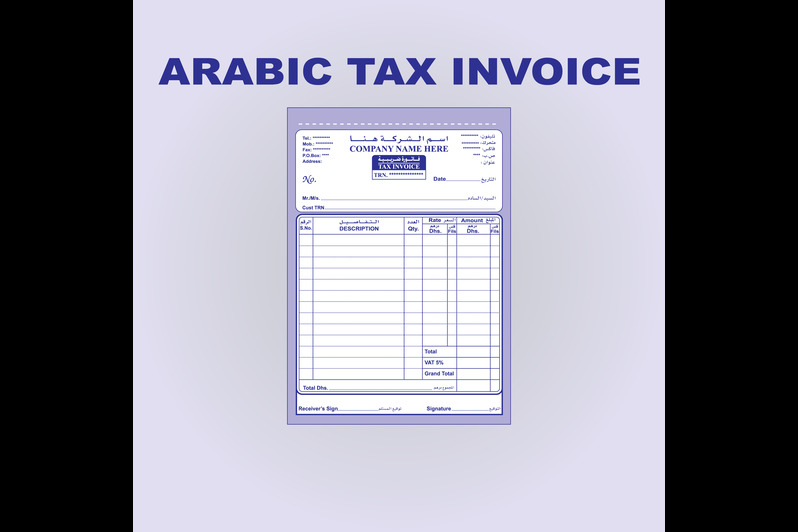

Simplified VAT invoices have to contain the following information:

- The label “Tax Invoice” presented visibly on the tax document

- The serial number of the tax invoice or a special number by which the tax invoice can be identified and arranged from among a group of invoices

- The tax registration number, name, and address of the tax-registered business supplying goods/services

- The date wherein goods/services are supplied by the taxable person

- Description of products/services supplied

- The price of each unit of service or good, in addition to the quantity and volume supplied, the tax rate, and the amount payable in AED

- The total amount is payable in AED

- Total VAT amount charged

- The value of the discount, if offered

VAT Regulations Article 59 provides a guide on the complete format for UAE VAT invoices. A supplier can plan the tax invoice, as well as organize it in accordance with the prerequisite. However, there have to be systems in place that can guarantee tax invoices contain all the information listed above.

FTA Public Clarification (VATP006) Re: VAT Invoices

The Federal Tax Authority of the UAE issued Public Clarification VAT P006. It addresses the requirements for the issuance of tax invoices. This includes the following points:

- It’s not acceptable for taxable persons to offer only the option of giving an invoice. A tax invoice has to be given in any circumstance wherein a supply is made

- Simplified tax invoices don’t need to show net value or value before tax for every line item

- Rounding on VAT invoices should be in the nearest Files (for line-item basis)

- When tax invoices are issued in foreign currencies, they must show tax amounts in AED

- Full or detailed tax invoices have to show tax value, including net value, for every line item

Read Also: How VAT in Oman Affects the Country

Detailed Tax Invoice Requirements in UAE

Under UAE VAT legislation, detailed tax invoices are to be issued by VAT-registrants for assessable goods or services supplied to other VAT-registered businesses. This is provided that the provisions surpass Dhs10,000. A detailed VAT invoice is often for merchants and wholesalers managing higher amounts of taxable supplies.

A VAT invoice in UAE must contain this information in English/Arabic:

- A unique invoice number (sequential, for identification purposes)

- The date on which a tax invoice was issued, plus the date of supply (if they’re different)

- Legal name, tax registration number, and address of the taxable person

- Legal name, tax identification number, and address of the customer

- Description, quantity, and type of sold goods or description of provided services

- To unite price for goods/services goods, excluding the VAT charge

- Rebates or discounts provided (not added in good/service’s unit price)

- Total VAT amount payable (must be in AED)

- Method for calculating the profit margin

- Method for calculating VAT (standard, exemption, or zero rates)

- The label “Tax Invoice” presented visibly on the tax document

Can Non-Register Businesses Issue VAT Invoices?

Non-registered businesses or persons for the purpose of VAT in the UAE are not allowed to create and issue VAT invoices. Unregistered persons are liable to pay a fine for issuing tax invoices. Do you need further information or clarification regarding VAT in the UAE? Call us here in VAT Registration in UAE today to talk to seasoned tax professionals!

FAQs: Tax Invoice Requirements

Q1. What should be the currency used in Tax invoices in UAE?

Q2. Should VAT invoices be issued for goods/services supplied to an unregistered person?

Q3. How long should VAT invoices be retained in the UAE?

Q4. What happens if a business fails to issue a proper VAT invoice?

Q5. Is VAT applicable on all invoices in the UAE?

Read Also: VAT Accounting in UAE